How to Invest in Circle Stock

![]()

Circle, one of blockchain’s biggest and most respected companies, is going public on the New York Stock Exchange.

It’s happening through a SPAC instead of an IPO: in plain English, this means that Circle will merge with Concord Acquisition Corp., another company that’s already publicly listed. This is a popular way for tech companies to “go public” without having to go through the rigamarole of an IPO. (Also, smart investors can get in early.)

For blockchain investors, what this means is you can buy Circle stock now, under the ticker CND. Note you’re not technically buying Circle stock, until the merger happens (which is estimated for Q4 2021). At that time, assuming the merger goes through, your CND will convert into CRCL, and be repriced accordingly.

In this brief, I’ll explain what Circle does, why you may want to invest now, and why you may want to wait. I’ll also discuss the home-run investment scenario for Circle that makes it particularly interesting for blockchain investors. (Full disclosure: our parent company Media Shower counts Circle as a client.)

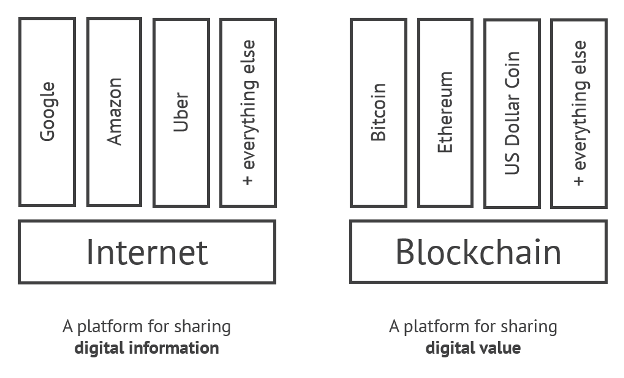

The Internet of Value

When we were interviewing Jeremy Allaire, Circle’s CEO, for our case study in Blockchain Success Stories, he likened the digital movement of money to the digital movement of information. Just as the Internet made it easier than ever to share digital information, the next iteration of the Internet would make it easier to share digital value.

This clicked for me. It actually seemed kind of obvious, if you thought about money as a product. If you could make money into a better product – faster, cheaper, easier to send – then more people would begin using your product. (Of course, the government controls the “product,” which makes things tricky. More on that below.)

Today, Circle’s primary product is USDC, the “digital dollar” that’s backed U.S. dollars. If you’re new to the space, USDC is a stablecoin, meaning it holds its value over time (as opposed to digital currencies like bitcoin, which are wildly volatile).

You put in one U.S. dollar, you get one USDC. Simple. Instant. Free.

With your USDC, you can now participate in the new digital economy of cryptocurrencies. You can now trade your USDC for BTC or ETH. You can store your USDC in DeFi platforms and earn “yield” (like interest). Think of USDC as an “on-ramp” or a “bridge” between the traditional economy and the digital economy. And it works: nearly $850 billion USDC have been transferred back and forth.

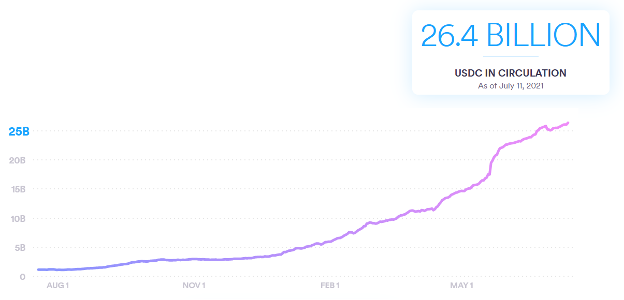

USDC is designed to always hold its price against the dollar, and it has done this remarkably well, especially as the amount of USDC has increased. And increase it has: there were about $4 billion USDC at the beginning of 2021; today there are over $25 billion. (Current stats here.)

Stablecoins serve an important role in the digital economy. For example, traders who are moving money between cryptocurrencies need a place to store their money between trades. Cashing bitcoin back into dollars is slow and expensive; USDC provides a stable store of value within the digital economy: a port of calm in a stormy ocean. This is why USDC has grown so quickly.

Unlike some other stablecoins, one USDC is backed one U.S. dollar. This is how Circle makes money: they are able to earn interest on the deposits, which makes the company a little bit like a bank.

In other ways, however, Circle is more like a tech company than a bank. It also makes money through a suite of tools and APIs that companies can use to build USDC functionality into their own financial systems, with Circle earning transaction fees. For example:

- If you want to pay vendors in crypto, you can use Circle’s tools to “switch” back and forth between traditional and digital dollars.

- If you want to invest part of your corporate treasury in crypto (like Tesla buying bitcoin), you can use Circle’s tools as an “on-ramp” and “off-ramp” between traditional and digital investments.

- If you want to offer DeFi products to customers, you can use Circle’s tools – powered USDC – to create white-label versions of, say, Compound.

As an investor, if you think this movement toward digital money is the way the world is bending, then Circle is worth a closer look.

Why You May Want to Invest

Experienced management team. Circle is led Jeremy Allaire, a serial entrepreneur with a track record of success: first with software company Allaire Corporation (which went public in 1999), then with online video platform Brightcove (which went public in 2012). Besides Allaire, Circle has invested heavily in its management team, funded in part a $440 million private investment round in May (!).

Long haul experience. Circle was founded in 2013, which in crypto years is like the Paleozoic Era. While Circle spent years wandering the wilderness (at one time they had a Venmo-like consumer payments app; at another time they owned the crypto exchange Poloniex), they have an unqualified hit on their hands with USDC.

Regulatory work. From the beginning, Circle decided to work within the system instead of outside the system (evolution, not revolution). For example, the company went state-to-state and applied for money transmitter licenses. It was the first company to receive New York’s infamously difficult BitLicense. This is hard, thankless work, but today Circle is the most licensed company in the industry.

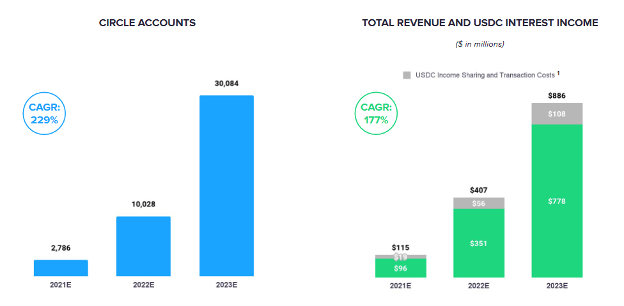

A $4.5 billion company. The current deal values the company at $4.5 billion, which means it will have plenty of cash (both traditional and digital) to fuel the company forward. Indeed, the company is planning for massive growth (and commensurate spending), as outlined in its investor presentation. If you think Circle has a head start, this war chest will make it even harder for competitors to catch up.

The business model. Again, you put U.S. dollars into your Circle account, and Circle gets use of those dollars. Unlike so many crypto projects that are basically playing with virtual currency (i.e., funny money), Circle has use of real U.S. dollars, like a bank. Again: it’s much more than a bank, which makes it hard to imagine how traditional banks will ever catch up.

Why You May Want to Wait and See

Financials. The Investor Presentation is light on financial details. Unlike Coinbase’s recent IPO filing, which listed past years of historical growth, Circle is only sharing estimated 2021-2023 numbers, which are basically projections. While the 2021 numbers are presumably based on half a year of actual results, an investor must take future financial projections with a big grain of salt. (No one knows.)

Pricing. Again, you can currently buy shares under ticker CND. But avoid the temptation of saying, “Coinbase is trading at over $200, CND is around $10 … to the moon baby!” SPAC don’t work like that. Instead, they generally trade around $10, and are then converted into the equivalent amound of CRCL if the deal goes through (see how SPACs work). You may want to wait for better price information.

Regulation. Federal Reserve Chairman Jerome Powell told the House Financial Services Committee this week that stablecoins – and their lack of regulation – are a concern for the Fed. “Really the question is stablecoins,” he said. “They’re growing incredibly fast, but without appropriate regulation.” If the Fed were to come in with heavy-handed regulation, that could spell trouble for Circle.

On the other hand, it might be an opportunity.

The Home-Run Investment Scenario

Powell went on to say, “You wouldn’t need cryptocurrencies if you had a digital U.S. currency.” Let that statement sink in.

This is perhaps the clearest signal yet that the U.S. is (finally) thinking seriously about its own Central Bank Digital Currency (CBDC), which could severely limit Circle’s ambitions. (If you have the choice between a government-issued stablecoin and a privately-issued stablecoin, you’ll probably go with the government’s.)

On the other hand, the U.S. is so far behind China in developing a CBDC that it’s hard to imagine how it can catch up. China started developing digital currencies in 2014, which in crypto years is like the Mesozoic era. It’s highly unlikely that the U.S. can develop its own CBDC technology, given the enormous head start one of its biggest rivals. (Plus, the government is not known for its tech-savvy: remember the botched rollout of Healthcare.gov?)

As the “digital currency wars” heat up, one likely option for the U.S. will simply be to partner with a private company that’s already developed the technology. (Think about spectrum auctions, where the government sells frequencies for private companies to use for telecommunications. The government doesn’t build out the telcos itself; it just manages the framework.)

If the U.S. government were to create a framework (i.e., regulations) for stablecoins, then allow public companies to create the digital dollar “product,” guess which company is positioned to take the lead?

Circle.

It’s true that Tether is the #1 stablecoin market cap, but the first line of Tether’s Wikipedia entry says it all: “Tether is a controversial cryptocurrency.” Some have questioned whether Tether really holds the dollar reserves it claims, along with other crippling controversies listed here. Anything’s possible, but it’s hard to see the U.S. government tethering itself to Tether.

To recap:

- Scenario #1: The U.S. develops its own CBDC. Probably bad for Circle, because it’s hard to compete with government money. (Though Circle could pivot into making its tools available to the new government-sponsored digital dollar.)

- Scenario #2: The U.S. partners with private companies to develop a CBDC. Probably great for Circle, because they’re the most likely candidate to make it happen at scale. (Though not the only candidate.)

Other scenarios are possible, of course, but I consider Scenario #2 likely. “Likely” does not mean “a done deal”: there’s a long row left to hoe. But if Scenario #2 comes to pass, then Circle becomes a home-run investment for the ages. Think about not only having a government contract, but having a government contract to run the government’s money. Great work if you can get it.

For me, Circle is a promising investment either way: I believe blockchain is the future of money, stablecoins are the infrastructure of blockchain, and Circle has the most reputable stablecoin. If the U.S. government were to somehow leverage USDC for a CBDC, then it’s a home-run investment, and I’d make a big bet on the company.

My personal decision, then, is to buy a little bit now, and watch how things evolve on the CBDC front to potentially buy a lot more later. Eventually, this may all come full circle.

I’m a highly respected and well-known author in the cryptocurrency field. I have been writing about Bitcoin, Ethereum, and other digital assets for over 5 years which has made me one of the most knowledgeable voices in the space. My work has appeared in major publications such as CoinDesk, Forbes, and The Wall Street Journal. In addition to my writing, I’m also an active investor and advisor in the cryptocurrency space.